Digital Transformation · Private Sector

Designing standardised advisory workflows with embedded compliance for a major bank

Overview

A New Zealand major bank with over 5,000 employees and serving 1.2 million customers required support to standardise advisory processes across departments while ensuring regulatory compliance without creating administrative burden.

The brief focused on designing user experience solutions using new platform technology that would address fragmented departmental approaches and improve operational efficiency. The engagement needed to balance regulatory adherence with usability whilst creating scalable workflows that improved both staff and customer experiences, starting with retail banking.

Outcome

Delivered a user-validated design for one of the bank's most complex customer advisory processes that successfully balanced regulatory compliance with operational usability. Created a scalable framework of four baseline scenarios with comprehensive implementation documentation endorsed by technical stakeholders for feasibility.

Impact

The embedded compliance approach serves as a centralised source of truth for customer advisory information, eliminating information silos that previously fragmented customer service. Starting with retail banking, this enables consistent customer service whilst reducing regulatory risk, accelerating staff training, improving adviser confidence, and creating more seamless customer interactions. The validated approach provides groundwork for scaling across all banking segments

My role

As the Strategic Designer in a four-person international team, I led cross-departmental alignment over 1.5 months to transform compliance from administrative process into helpful conversation guidance. I facilitated stakeholder engagement across compliance, business, and technical teams, delivering user flows, wireframes, and process standardisation that configured Salesforce functionality to meet business requirements and regulatory standards.

The Full Story

Fragmented processes create opportunities for improvement

The bank was implementing Salesforce technology as part of their multi-year digital transformation, with customer advisory processes identified as a key area for enhancement within the first phase. Each department had developed separate approaches to customer needs analysis and regulatory capture under Credit Contracts and Consumer Finance Act (CCCFA), Financial Markets Conduct Act, and other financial services legislation. This highlighted two key challenges:

Advisers lacked unified customer context and a centralised source of truth, working with information scattered across multiple systems with constant 'swivel chair' navigation between applications.

For example: Advisers sometimes needed to search different systems for recent account activity during customer conversations, and some had developed informal note-taking approaches because existing systems had limited relationship context capture. Business banking prospects expected seamless credit applications that didn't require repeating information across multiple systems, and private banking clients expected their relationship manager to know about their recent business loan before discussing investment strategies.

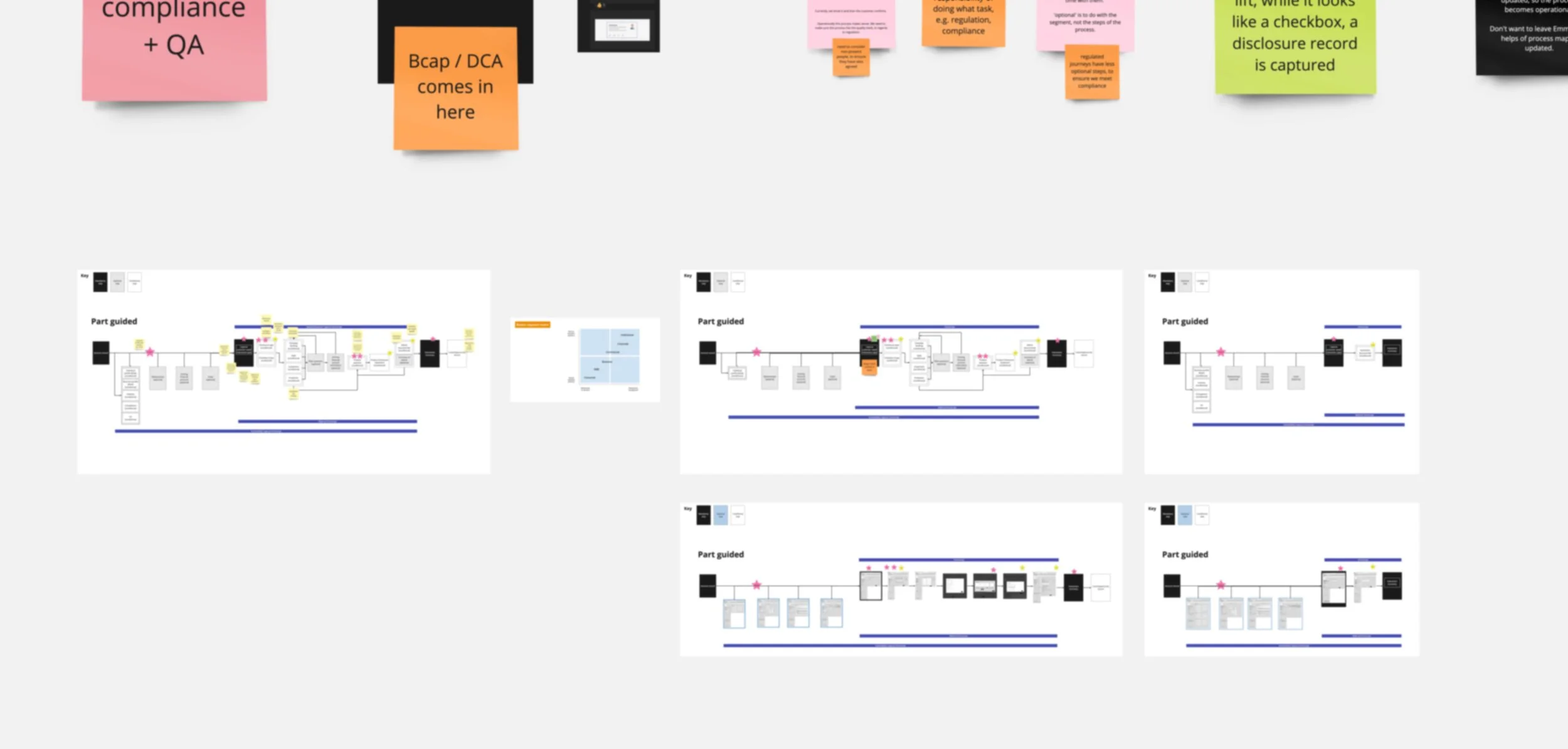

Departmental approaches to compliance varied significantly, creating inconsistency and effort duplication that reduced time available for customer engagement.

For example: Retail banking used straightforward guidance while private banking focused on sophisticated wealth planning conversations, but both needed to meet similar core regulatory requirements—including customer needs analysis, risk assessment, and suitability obligations—through different processes.

Approach

* Please note that the images have been blurred intentionally to protect client confidentiality.

Turning regulatory burden into conversation guidance

When we started planning how to configure the platform for customer advisory processes, we quickly realised this wasn't just a technology implementation—it was an opportunity to rethink how compliance could work within the business. Rather than treating regulatory requirements as something to endure, we saw a chance to make compliance helpful, transforming administrative burden into guidance that advisers would want to use.

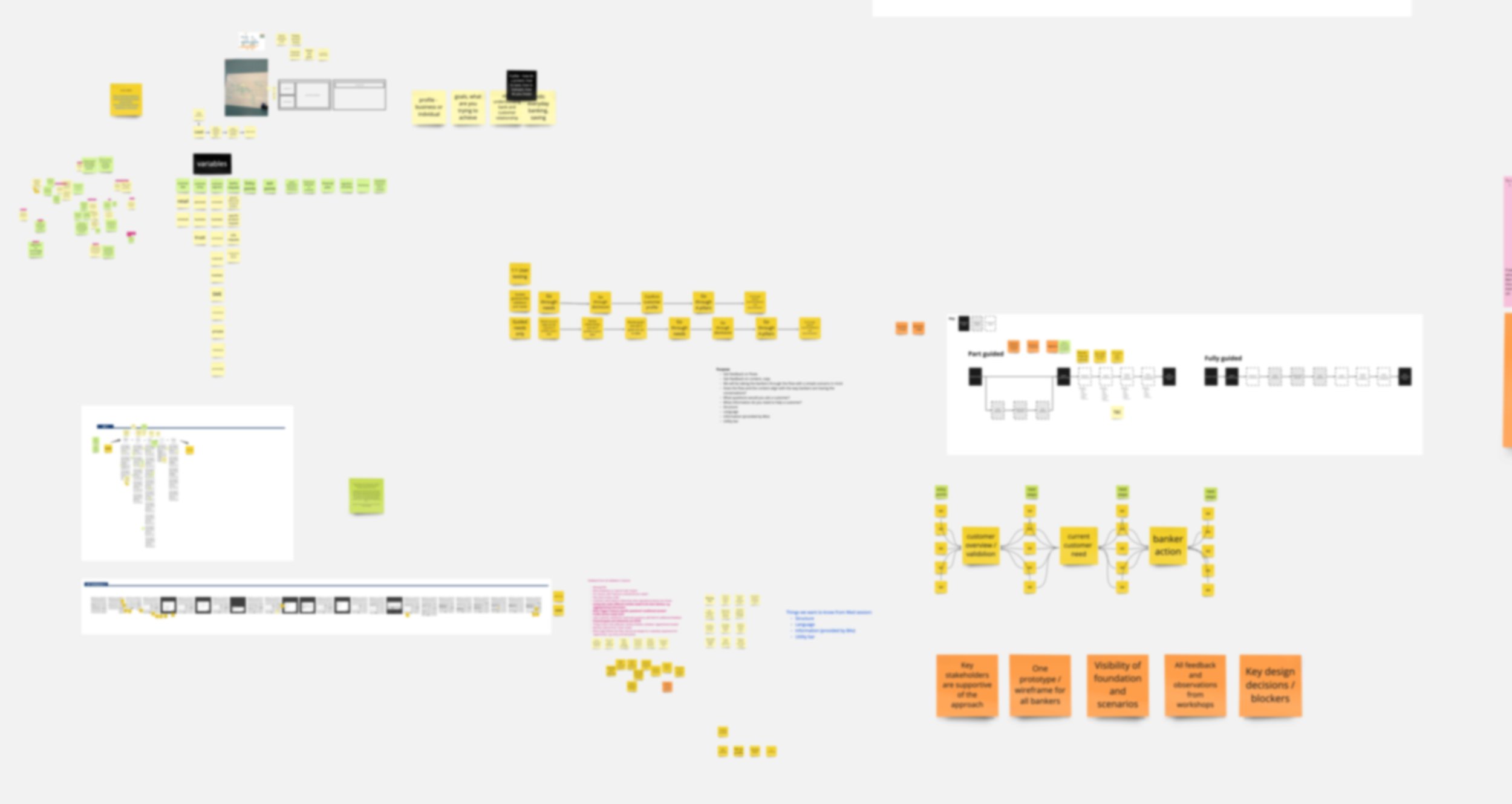

Step 1: Three paths, one strategic choice

Early analysis of the platform's capabilities and the bank's requirements revealed that we needed to make a fundamental decision about how compliance would be handled. Through stakeholder discussions and platform exploration, we identified three distinct paths the implementation could take:

Compliance-first: Put regulatory requirements front and centre, guaranteeing adherence but creating cumbersome experiences

Department-specific: Let each segment configure according to existing practices, maintaining familiarity but continuing current process variations

Embedded design: Create standardised workflows using guided conversations that naturally capture regulatory requirements

We advocated for embedded design because it addressed the core brief whilst transforming the staff experience. Rather than forcing advisers to think about compliance as separate work, embedded design would reduce mental load by making regulatory capture feel like natural conversation guidance that actually helped them serve customers better and feel more confident in advisory conversations.

Working space to understand process variations across business segments

Step 2: Four scenarios, not one-size-fits-all

Each banking segment had legitimate reasons for their different approaches. Institutional clients needed complex deal structuring, private banking customers required sophisticated wealth planning, business clients focused on commercial growth strategies, and retail customers needed straightforward personal guidance.

We developed four baseline scenarios tailored to these segments, creating a modular approach that managed existing complexity whilst laying groundwork for future scalability.

Understanding ideal workflows and how regulatory requirements might surface in conversations

Step 4: Designing wireframes with embedded compliance

Through rapid sprint cycles, we refined the early wireframes into detailed designs that embedded compliance naturally into conversation flows. Using Salesforce's out-of-the-box Lightning components, we ensured designs could be implemented without custom development. We positioned compliance questions within natural conversation flow, made key customer information immediately visible, and designed interfaces that could flex between different conversation types using progressive disclosure to reveal regulatory requirements as they became relevant to the discussion.

We also developed conversation frameworks for different customer types: prospective customers requiring full needs analysis, returning customers with updated circumstances, complex family situations, and business customers expanding into personal banking services. We considered information architecture: customer overview panels, information organisation, alert visibility, and how advisers could edit information as conversations evolved. Staff would need functionality extending beyond advisory sessions—setting reminders, emailing disclosures, and other relationship management functions.

Step 3: Understanding conversations, not forms

Rather than beginning with user interfaces, we started with understanding how advisory conversations typically flow: what advisers need to know, questions they ask to suggest products, and compliance requirements for record keeping. Through collaborative working sessions with the client, we translated these natural conversation patterns into early wireframes and process flows.

The breakthrough was identifying which regulatory steps were truly critical versus habit. This let us strike a careful balance between compliance obligations and operational flexibility.

Iteration of wireframes and mapping of compliance met across different user paths

Step 5: Reality-testing with retail advisers

Starting with retail customers due to the technical release rollout, we developed scenarios covering different user journeys from streamlined 'happy path' interactions to complex cases requiring sophisticated regulatory assessment. We ran 15 one-on-one virtual usability testing sessions with retail advisors using the scenarios, focusing on navigation flow, field terminology, and mandatory vs optional data capture.

The testing revealed unexpected insights about how system limitations affected both staff confidence and customer experience. One adviser mentioned they'd been creating workarounds because they couldn't see customer vulnerability alerts in another system. They'd discovered this during awkward conversations that could have been completely avoided—situations that left both customers and staff frustrated. The kind of insight that only comes from watching real work happen.

We also discovered interface preferences that supported better standardisation. Drop-down menus worked far better than free text fields for standard information—advisers were naturally more consistent when selecting from options rather than typing their own descriptions. We limited free text to prevent different note-taking styles from undermining standardisation.

Based on this feedback, we refined the wireframes to improve alert visibility, streamlined the customer overview panel to show what advisers actually needed, and restructured information organization to match their expectations.

Wireframe prototype

Step 6: Proving it could scale

After refining the design based on retail adviser feedback, we needed to validate that the approach would work across all segments before broader implementation. We conducted Subject Matter Expert validation sessions to test whether it could handle different advisory scenarios whilst maintaining consistency.

We stress-tested the design with complex scenarios—private banking customers with multiple mortgages, rental income streams, and sophisticated CCCFA assessment requirements. The modular design proved flexible enough to accommodate different advisory types across all segments.

Technical experts validated the solution for scalability, feasibility, and regulatory soundness. With Subject Matter Expert approval and technical sign-off, stakeholders had confidence it could scale beyond retail implementation.

Step 7: Setting up for success

The handoff stage often determines whether great design becomes great implementation, but we didn't wait until the end to involve technical experts. From early on, we worked with Business and Technical Analysts to understand what the platform could and couldn't do. This shaped our design decisions from the start rather than creating problems later.

By final handoff, we'd created comprehensive documentation that anticipated the development team's questions and provided clear guidance for tricky edge cases. This upfront collaboration meant development could move fast without the usual delays when design meets technical reality.

Final report detailing design framework, scenarios, conversation framework, wireframes and user testing insights

Deliverables

-

Usability testing report with findings and recommendations from 15 frontline banking staff across four departments

Synthesis of feedback on language, screen organisation, and workflow preferences

-

Wireframes and screen layouts for different customer types including new prospects, existing customers, and complex family situations

Conversation frameworks accommodating institutional, private, business, and retail banking scenarios

-

Comprehensive requirements documentation with clear, actionable guidance for development teams

Technical validation report confirming feasibility, scalability, and regulatory compliance

Structured handoff process documentation

Outcomes

Compliance feels natural rather than burdensome for retail advisers

Transformed regulatory requirements into conversation guidance for retail banking, enabling advisers to focus on customer relationships whilst capturing what regulators required. Staff experience compliance as helpful prompts rather than separate administrative work.

Enhanced staff confidence and customer experience

Advisers reported feeling more prepared and confident in customer conversations, with seamless access to relevant information enabling them to focus on relationship-building rather than system navigation. Customers experienced more informed, uninterrupted conversations without awkward pauses for information gathering.

Created operational consistency across segments

Developed a scalable solution validated across banking segments that reduces fragmented approaches whilst respecting legitimate differences in advisory complexity. Retail implementation demonstrated better customer context and more consistent processes that reduce training time.

Supported leadership confidence in scaling decisions

Technical validation and subject matter expert approval across all segments provided stakeholders with evidence that the solution could scale beyond retail before committing to broader development, supporting informed rollout decisions based on user validation rather than assumptions.

Learnings

Constraints often contain the solution

Instead of treating regulatory requirements as unavoidable friction, we discovered they often overlap with what good advisers naturally do. Questions advisers ask to understand customer circumstances and assess risk happen to be exactly what regulators want documented. Rather than adding compliance as separate administrative work, we designed it as helpful conversation structure—risk assessment prompts became better customer understanding tools, documentation requirements became useful decision records for future reference.

Modular approaches manage complexity without sacrificing consistency

Rather than forcing uniformity or accepting fragmentation, we found commonalities and differences across departments and designed baseline scenarios with modular components. This accommodated legitimate departmental variations whilst establishing consistent foundations for future scaling. The modular approach also broke down complex work into manageable pieces for the team, making the project more efficient to execute.

Designing UX doesn't mean giving users everything they want

We balanced adviser preferences for flexibility with standardisation needs for consistent documentation and compliance. The strongest design decisions came from understanding where user desires and business requirements diverged, then finding elegant compromises that felt natural while meeting regulatory objectives.